#2 Indian SMBs & The Case for 'Thin' SaaS

#2 Indian SMBs & The Case for 'Thin' SaaS

'Thin' SaaS might just sit at the right intersection of scale and profitability

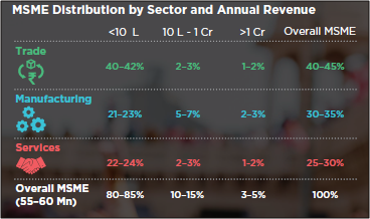

The Indian SMB space is much talked about as a major business opportunity. All estimates put the number of SMBs in the country at over 50 million at the least. This large base of merchants is heterogeneous as it gets. There is a broad classification I want to lead with before I get to the specifics.

India’s strength in the trade businesses stands out. For the purpose of this discussion, I am keeping manufacturing out of the purview. (Reasons: Fixed buyers and sellers, low frequency, high ticket size transactions. All of these ensure fixed business practices)

Also, a whopping 94% of these businesses are registered as sole proprietorships which points to them being mostly unorganized.

More than 90% of these businesses are in the “S” of SMBs. Small in terms of revenue and the size of the organization.

It is this set of merchants that is going to be the focus of this article. The small establishments run by small teams with a single owner/few partner owners. They are the segment where the true potential for a lot of innovation lies. In terms of metrics, revenue and team size help us categorize these businesses. Annual revenue of less than 20 Cr. and/or team size less than 20 people in the business, is my line in the sand, but you get the drift.

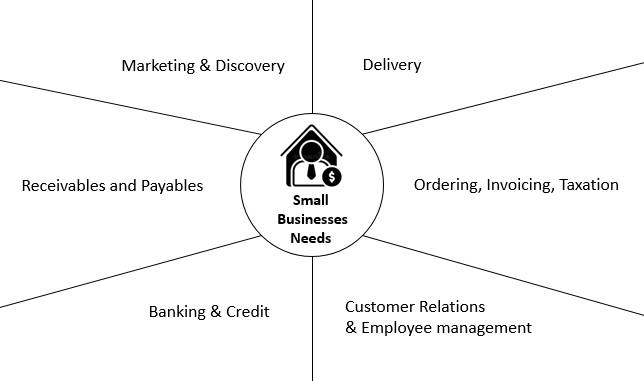

What follows, is a rundown of their needs, behaviors, and how one segment of their needs is witnessing huge interest and how that will pave the way for a new kind of “Thin” SaaS product solutions. Let’s begin with an overview of the needs of small businesses.

Marketing & Discovery: This happens via a bunch of ways including word of mouth, offline branding, listing on industry-specific aggregators like Zomato, Swiggy, Amazon, Flipkart, etc. Whatsapp is also a powerful medium. The merchant can also decide to create a simple website using Shopmatic, Wix, Shopify(more useful for larger merchants because of the fee associated).

There can be a clear distinction. Marketing on owned platforms builds an identity and brand. Listing on other platforms creates discovery and sales.

Receivables and Payables: This is a space that has seen the most active change and digitization in the past few years. More on this later.

Ordering, Invoicing, Taxation: These are managed on legacy ERP/taxation tools. In fact, India has more than 300 local players creating ERP solutions for specific industries. These tend to be brute solutions that get the job done, not the prettiest to look at or the easiest to navigate and learn.

Sales are through local partners who do training/installation/customer care on behalf of the firm that created them. Most solutions are not cloud-based. On the taxation side, Tally is one of the clear winners out of the crowd.

However, for a lot of merchants, a lot of these operations are also managed over excel + email. Spreadsheets are still a powerful play.

Customer relations and employee management: Customer relationship management is perhaps one of the most broken spaces for merchants. Communication is over mail/SMS/WhatsApp with poor messaging and ill-defined frequency. Excel is also a common tool used here. To add to that, in a lot of businesses, CRM is a non-existent process. Employee management is a lesser of concern for these merchants. (few employees, low salaries, limited or no compliance, demand-supply skewed in the favor of the business)

Banking & credit: Credit records are mostly maintained over manual ledgers (both customer credit and credit from suppliers). Mostly banking portals are robust to support use cases or the use cases are managed through close relationships with the bank manager/key account manager. COVID is now moving the needle as merchants look for better and more expansive experiences from online bank portals.

In all these areas, using solutions that help growth are more preferred to solutions that drive efficiency first. As a mindset, merchants think clearly that:

Growth > Efficiency

Adoption of efficiency enabling solutions is driven by external stakeholders:

Customers

Influencers

Government regulations

One of the key reasons that efficiency gets lesser preference is because manpower is cheap so work can be done manually till scale is manageable. The teams are small and staffed by semi-skilled workers, mostly known well to the merchant. In most cases, they multi-task a lot inside the business thus recovering their cost.

Out of all these, one particular segment of services which has seen heavy change in the last few years has been payments(Receivables and Payables). The wave that was started by demonetization was followed up by the government directly getting involved by launching UPI (which crossed over 1 bn transactions in May!). The list of active players is long and is littered with all the major names and includes all major banks, the government, and private players.

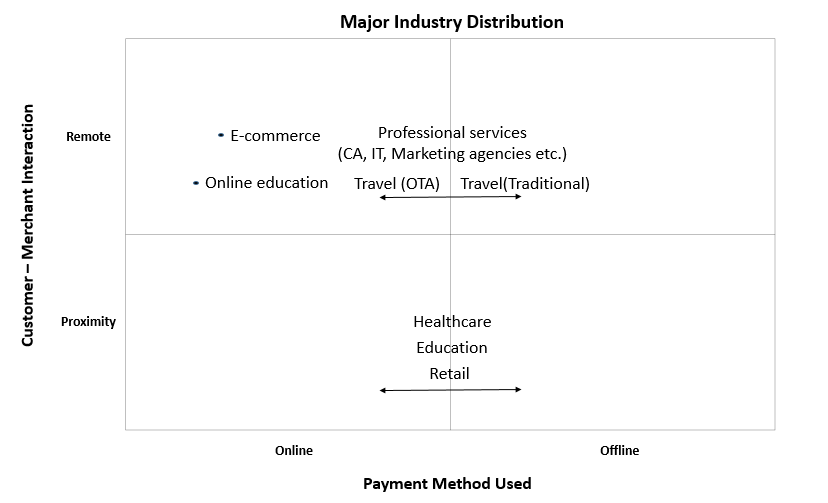

When I started out working in the payments industry, I formed a framework that has been my go-to way of looking at how payments interact with the business and what has the evolution been like in the payments space. Firstly let’s look at how our small businesses fit into that matrix from an industry perspective.

The industries above cover a huge chunk of transactions out of the total transactions carried out. A merchant can play in different quadrants of the same time by having a hybrid business model.

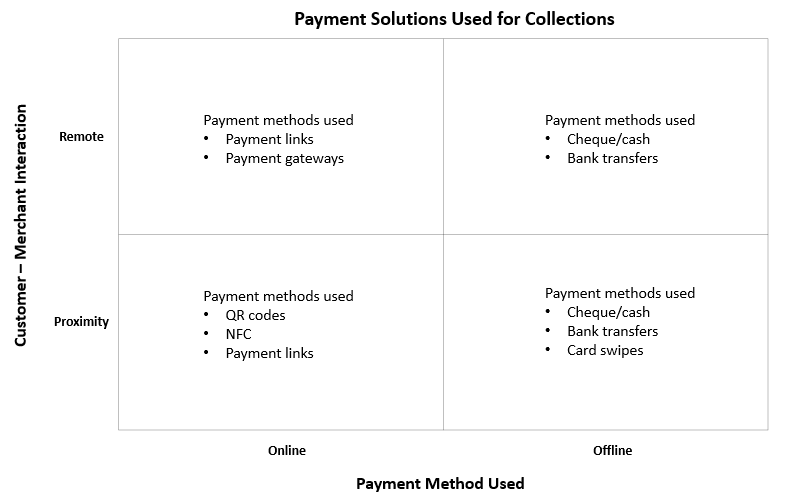

Increasingly the shift is to the upper 2 quadrants with business interactions going remote. This in turn powers more digital transactions. Even the strongly proximity driven industries like retail are moving to online transactions. The bottom left and top left quadrants are getting filled now. Coming to what payment solutions exist in these segments, here is a quick high-level overview.

(Note: I have classified a payment mode as offline if it involves a physical/offline interaction. E.g. for a bank transfer, the merchant has to share his/her bank details with the consumer over message followed by adding a beneficiary)

For each of these quadrants, there are payments players spread out in terms of product capabilities. Take PayU, for example, it has options ranging from a QR code in a shop to a payment gateway on a website (this is the screen you see at the end of all online transactions, asking you to pick your preferred payment method).

What this really has meant for the merchants is that for the first time, a function that is not directly linked to the growth of the business is getting strongly digitized. You can track your orders, their payments, customer details from within one neat solution that does just that for you. All of this coupled with some revolutionary upgrades in digital on-boarding and customer issue handling.

Payments is the beachhead that companies have been able to establish and it is a fantastic use case to go after because:

It is a high-frequency activity, multiple exposures in the day for a merchant to the app/web dashboard driving comfort and behavioral change

It is a critical and core activity of the business and if you have trust built up in that segment, it is easier to nudge the merchant to adopt other digital solutions

Payments, however, is not a sustainable moat for firms. The cost of the acquisition remains high on both sides with cashback and margins are wafer-thin. Sales team structures are also cost heavy. On a single transaction, a payments firm makes revenue in the range of 1-2% and a gross margin which is even lower. UPI and Debit card transactions are nearly free. It is natural to look for additional avenues and credit is a logical next step most are moving to. But there is more to be done.

Extending this idea forward of a neat solution to address a critical enough need, I strongly believe that merchants stand to benefit from similarly built light SaaS solutions built for the following efficiency first needs with payments added in.

Ordering, Invoicing, Taxation

Banking & Credit

Customer Relationship Management

But these solutions have to be extremely light to use, build, and maintain for the following reasons:

You only make money from small businesses at scale because attrition is high and the value realized per merchant is less. A complex solution requires training and increases attrition.

A complex solution does not make viral/word of mouth/referral marketing easy thus slowing the pace of adoption.

The businesses are run by single owners with small not semi-skilled teams. Remember you occupy a very tine share of mind for the business owner. You can’t rely on muscle memory to form and increase adoption. Make it simple and intuitive first.

Building a light solution allows you to keep lean engineering and sales teams and cost structure.

Let me pause for a bit and define a term that covers all that I said above, The term is “Thin” SaaS.

“Thin” SaaS refers to a simplified solution which adds sufficient value that a business can self on-board, self-train on and enjoys viral adoption & retention backed by little to zero sales & account management

This is the solution that firms have to build to derive value out of the market. Some key tips on how this can be done and is being done today by a few pioneers. Focussed on just a few players, the list is not exhaustive, focus is on the points to keep in mind.

Payments firms were the first to go down this route. As they look to add solutions to beef up the stack, it will be interesting to watch how they can keep being “Thin” at the heart of it.

Drive a low monetization, high engagement use case first. A beautiful way this has been done is by Khatabook. Khatabook allows merchants to keep track of credit given out to customers in an easy to maintain digital format. It has crossed 10mn app installs to date with great MAUs reported.

Another player that just came out with a similar offering is Smolcoach with its offerings for creators to take bookings and collect payments. In fact, Substack is a similar tool for writers. Look to bundle solutions that add sufficient value and yet keep the value proposition simple enough.

The banking space is also seeing a lot of action with a host of new players looking to develop Neobanks that will help to ease banking management and solve niche uses cases for small businesses.

Another firm that is solving this right is Refrens, a solution that allows businesses to create detailed invoices easily and collect payments.

Don’t think of this is as stripping down functionalities from enterprise solutions and offering that to small businesses. It has to be a ground-up genuine problem-solving effort based on first principles thinking.

When thinking of adding a new use case on top of the original offering, make sure that it is joint at the hip. Build that new feature in-house(if you can) and not through partnerships as you would want to control the experience closely for every feature addition.

Rely a lot on user-generated content to promote the product. Work with influencers/super users to allow them to create easy to understand vernacular content to market the product. This is stronger than a testimonial exercise. This is putting in place a positive loop that is generated by user content generation, distribution, and engagement.

Refrain from going all out and building in each and every feature request on top of the light initial offering. Minimalism is at the heart of it for a variety of reasons.

The approach does not have to be to cover all use cases that conventional solutions covers, by building one block at a time. Solve for a set of composite problems and create elegant API solutions so that the information on your system can be easily consumed by let’s say a Tally partner to build a plug-in for Tally.

In the end, all efficiency first activities drive growth in terms of cost savings and revenue enhancements but the value of that has to be constantly reinforced to the merchants in terms of showing them hours saved, money saved, users retained, etc. Define the set of metrics that will reinforce these values for the businesses and showcase them well.

A challenge that has to be answered though is creating enough revenue streams and then after deciding the revenue streams, fixing the pricing model, and ensuring seamless payments collection from merchants. Fintech with lending, insurance, and payments will be monetization layer on top of all solutions.

But “Thin” SaaS is the model to build on when going after the huge SMB market in the country. There are emerging proofs of that and the asset-light build model that it allows firms to have in place will be a great attraction. This just might be the route that creates profitability for firms in the SMB space. I will be tracking its movement keenly.

I hope you liked the article and the views I had to share! I would love to hear more from you or just drop in to say Hi!

Very well written piece on Indian SMBs. Totally resonates with our perception and approach at Vendosmart.com

Well articulated thesis,

"This is stronger than a testimonial exercise. This is putting in place a positive loop that is generated by user content generation, distribution, and engagement"

- how to cross the chasm where value creation becomes positive loop, any examples w/ the metrics that were optimized to generate the positive loop